"RBI 0.25% rate cut: Why Urjit Patel's Diwali bonanza may not ease EMI burden")

Reserve Bank of India (RBI) governor, Urjit Patel, on Tuesday announced a 25 bps cut in the central bank’s repo rate -the rate at which the RBI lends to banks, to a six year low of 6.25 percent. This is the first policy from the RBI which is actually set by a monetary policy committee (MPC). Logically, stock markets, home and auto loan borrowers cheered the move seeing this as Patel’s Diwali gift. But, does this 0.25 percent rate cut really mean anything to borrowers?

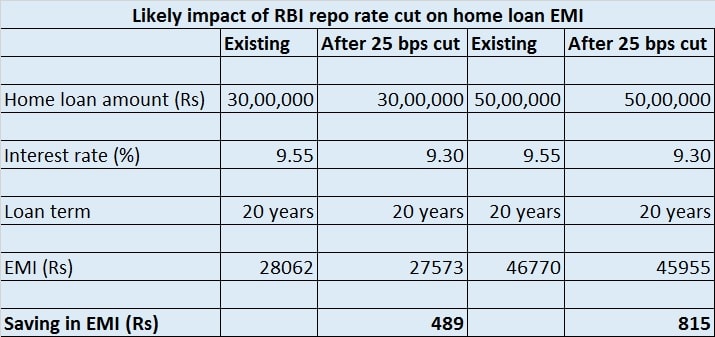

Let’s take a closer look at the actual impact of the quarter percentage point from RBI on your EMIs. In case, the banks decide to take the RBI rate signal and pass on the interest benefit to you, here’s how the math works out on your monthly EMI burden.

Take a look at this example. If you have an existing home loan of Rs 50 lakh payable over a 20-year-period, at the current rate of, say 9.55 percent interest, you would be paying an EMI of Rs 46,770. If the banks decide to pass on the rate cut to you through an identical 0.25 percent, your rate of interest on loan will fall to 9.30 percent. Then, your EMI payable would reduce to Rs 45,955 per month, giving you a monthly saving of Rs 815.

Similarly, if it is a Rs 30 lakh loan with a 20 year maturity, at a prevailing interest rate of 9.55 percent, you would be paying Rs 28,062 per month. Going by the same calculation, the EMI burden will now come down to Rs 27,573. In other words, you are getting a monthly relief of Rs 489.

The question is to what extent someone who is paying a substantial EMI to his bank every month benefits with a a few hundred rupees decline in his burden. Even more, it is difficult to imagine someone will take a new home loan looking at this few hundred rupees less EMI. What it means is that a 0.25 percent rate cut from the RBI ultimately doesn’t really benefit the end-consumer.

Now, all the above calculation is based on the assumption that the banks will indeed pass on the RBI rate cut to you, the customer, with a quick reduction in the lending rate. Going by past experience, it is very unlikely that lenders will do so. The simple reason is beyond RBI rate signals, there are a few other factors that has been playing a decisive role in guiding the bank lending rates in recent years. Of them, the biggest factor is the bad loan issue that has been troubling the banking sector. The second factor-high small savings rate in the economy–too has been acting as an impediment.

This is because banks need to first cut their deposit rates before slashing their lending rates. Doing so was difficult because of high small savings rate and banks risked losing their depositors to these schemes. But, with the government reducing small savings rate, banks now have more room to pass on the rate. The government had last week reduced the interest rates on small savings schemes by 0.1 per cent for the October- December quarter of the 2016-17 fiscal. The schemes include Public Provident Fund, Kisan Vikas Patra, and Sukanya Samriddhi Account.

Even the RBI has been pushing banks to pass on the rate benefits to the end consumer more effectively by changing the base rate calculation methodology to marginal-cost based model. In today’s policy too, the RBI has prodded banks to pass on the rate cut to consumers. “The easy liquidity conditions engendered by the Reserve Bank’s operations should also enable the smooth transmission of the policy action through various market segments. Furthermore, banks should find added impetus for better transmission by the recent downward adjustment in small savings rates,” the RBI said.

Having said this, the RBI rate cut is sentimentally a positive signal to individual consumers and industries. This probably signals the start of a lower interest rate regime. The point, however, is a 0.25 percent rate cut per se, may not benefit the customer immediately.

(Data contributed by Kishor Kadam)

"CloudSEK alerts Indian agencies of app Chinese handlers use to manage Indian scammers")

"Finance Minister Sitharaman tells RBI, regulators to meet fintech startups every month following Paytm fiasco")

"Head-on | From West to India, reversing the brain drain")

"Bankers, other likely buyers of Paytm Payments Bank want to redo KYC of all merchants, vendors")

"CloudSEK alerts Indian agencies of app Chinese handlers use to manage Indian scammers")

"Finance Minister Sitharaman tells RBI, regulators to meet fintech startups every month following Paytm fiasco")

"Head-on | From West to India, reversing the brain drain")

"Bankers, other likely buyers of Paytm Payments Bank want to redo KYC of all merchants, vendors")