- News

- Business News

- India Business News

- Fund houses line up FMP issues

Trending

This story is from March 5, 2014

Fund houses line up FMP issues

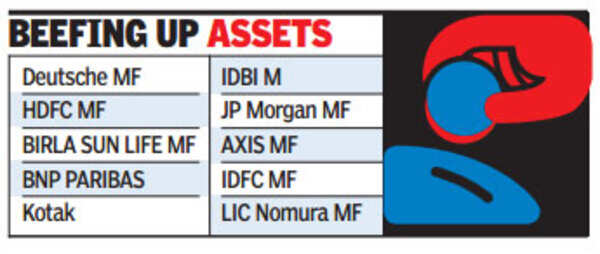

The coming weeks will see a surge in fixed maturity plan issues by mutual funds.Almost every large fund house has drawn up plans for an FMP in a hope to beef up assets under management.

MUMBAI: The coming weeks will see a surge in fixed maturity plan issues by mutual funds. Almost every large fund house has drawn up plans for an FMP in a hope to beef up assets under management. One of the major advantages of investing in an FMP is that for tax purposes, returns can be adjusted for inflation. Considering that RBI has forecast 6% inflation by January 2015, investors can avoid an income tax liability in an FMP with double indexation benefit, which makes it virtually a tax-free investment.

The double-indexation benefit is a tax loophole which allows investors to claim indexation benefit on an investment across two fiscals, even if the tenure of the mutual fund is only 370 days. This is how it works: If a fund is launched towards the end of March 2014 and has a maturity of 370 days, the scheme will be redeemed only in April 2016. This will result in the purchase and sale being spread over two financial years, allowing the investor to take advantage of adjusting returns for inflation for two financial years.

"March is also a time when there is tightness in the money market because of advance tax payments to the government. This gives mutual funds an opportunity to invest in certificate of deposits (CDs), which provide a return of up to 9.8%," said Nilesh Sathe, CEO, LIC Mutual Fund. Besides CDs, several top-rated corporates offer high returns on commercial papers. Since FMPs are close-ended, MFs can come up with NFOs, which allow for more intensive marketing rather that sell through distributors.

Although FMPs have much lower fee earnings compared to equity funds or long-term funds, the volumes are very high as investors see these as a substitute for fixed deposits. Investors have the option to choose the income or growth option. In the income option, returns are taxed at 12.5%. But in the growth option, a long-term capital gains tax of 20% is applicable if the investor chooses to offset his return against inflation (indexation benefit). Without the indexation benefit, capital gains tax of 10% is applicable.

Although FMPs are targeted at fixed deposit investors, there is an element of credit risk as highly rated companies have also slipped suddenly into default. But such defaults are rare and investments in CDs of public sector banks are considered risk free by mutual funds. UBI, the only distressed public sector bank, has also redeemed its CDs in time despite its problem with bad loans.

The double-indexation benefit is a tax loophole which allows investors to claim indexation benefit on an investment across two fiscals, even if the tenure of the mutual fund is only 370 days. This is how it works: If a fund is launched towards the end of March 2014 and has a maturity of 370 days, the scheme will be redeemed only in April 2016. This will result in the purchase and sale being spread over two financial years, allowing the investor to take advantage of adjusting returns for inflation for two financial years.

"March is also a time when there is tightness in the money market because of advance tax payments to the government. This gives mutual funds an opportunity to invest in certificate of deposits (CDs), which provide a return of up to 9.8%," said Nilesh Sathe, CEO, LIC Mutual Fund. Besides CDs, several top-rated corporates offer high returns on commercial papers. Since FMPs are close-ended, MFs can come up with NFOs, which allow for more intensive marketing rather that sell through distributors.

Last financial year, over Rs 70,000 crore was raised through FMPs - much lower than the Rs 1.3-lakh crore raised in FY12. This year mutual funds are hoping to better last fiscal's collections if yields rise in mid-March.

Although FMPs have much lower fee earnings compared to equity funds or long-term funds, the volumes are very high as investors see these as a substitute for fixed deposits. Investors have the option to choose the income or growth option. In the income option, returns are taxed at 12.5%. But in the growth option, a long-term capital gains tax of 20% is applicable if the investor chooses to offset his return against inflation (indexation benefit). Without the indexation benefit, capital gains tax of 10% is applicable.

Although FMPs are targeted at fixed deposit investors, there is an element of credit risk as highly rated companies have also slipped suddenly into default. But such defaults are rare and investments in CDs of public sector banks are considered risk free by mutual funds. UBI, the only distressed public sector bank, has also redeemed its CDs in time despite its problem with bad loans.

End of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- 'US safe country, cares deeply for well-being of Indian students': Garcetti

- 'Any effort to weaken India's progress has to be nipped in bud': SC judge in VVPAT case

- Explained: Inheritance tax - ‘promise’ that landed Cong in trouble

- Lok Sabha elections: 60.98% total voter turnout recorded till 7 pm

- 'RCB won't win IPL title until...'

- 'Will this country now work as per Sharia?': Shah slams Cong manifesto

- No jobs, no future: In Canada, drugs are Indian students’ last resort

- 'Right to privacy not absolute': Delhi HC to WhatsApp

- IPL Live: KKR set for mammoth total vs Punjab Kings

- Kerala election: 65.26% voter turnout till 6 pm

Popular Categories

Hot on the Web

Top Trends

PBKS vs KKR Live ScoreLok Sabha Election 2024 Phase 2Kerala Lok Sabha Election Phase 2Bengaluru Lok Sabha ElectionLok Sabha Election Phase 2 Full ScheduleDelhi Lok Sabha Election ScheduleKKR vs PBKS Match PredictionJEE MainsRajasthan Lok Sabha ElectionStock Market TodayIPL Orange Cap 2024IPL Purple Cap 2024IPL 2024 ScheduleLok Sabha Election Full ScheduleIPL Points TableIPL Match Full Schedule

Trending Topics

Ravi KishanEverest MasalaOptical IllusionRuslaan Movie ReviewMonthly Health HoroscopeShekhar SumanGurucharan Singh Missing NewsMonthly Career HoroscopeGovindaDance DeewaneRaw MangoShriya PilgaonkarArchana Puran SinghRadhika MerchantTik Tok Ban In USPreity ZintaBest Affordable Vacuum CleanersBest Headphones Under 1000Best Phones Under 35000Best Tv Of 2024

Living and entertainment

Latest News

Our minds have turned against usIf Virat opens, India can include both Rinku and Shivam in playing XI: Irfan PathanMore verification, more trust, better democracyLara Dutta reveals Akshay Kumar got scared as she thrashed a stranger who touched her inappropriately during the music launch of 'Andaaz'Best Superhero Tshirts for Women To Unleash Your Inner HeroVoter turnout: How Bengaluru's 'billionaires' street defied stereotypes?Voter turnout: How Bengaluru's 'billionaires' street defied stereotypes?Voter turnout: How Bengaluru's 'billionaires' street defied stereotypes?NVS Navodaya Vidyalaya Samiti Recruitment 2024: Apply for 1,377 posts till April 30, direct link hereLiving the high lifeVictory, the child of determinationAdani provides Dos and Donts to use electricity wisely during summer seasonElection Commission books BJP MP Tejasvi Surya for 'soliciting votes on ground of religion'Golden Days: When the iconic and humble actor Shashi Kapoor said NO to the National Award because he felt his work was not competent enough5 Times Vidya Balan Gave Us Indian Wedding Saree GoalsBhagya Lakshmi’s Aishwarya Khare gifts herself a solo trip on her birthday, says 'Going to Seychelles was on my bucket list'Amid AAP’s worst crisis, why is Kejriwal’s close aide Raghav Chadha missing?'Avengers 5': Benedict Cumberbatch, Tom Holland and other actors clear schedules for January 2025 shoot

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service